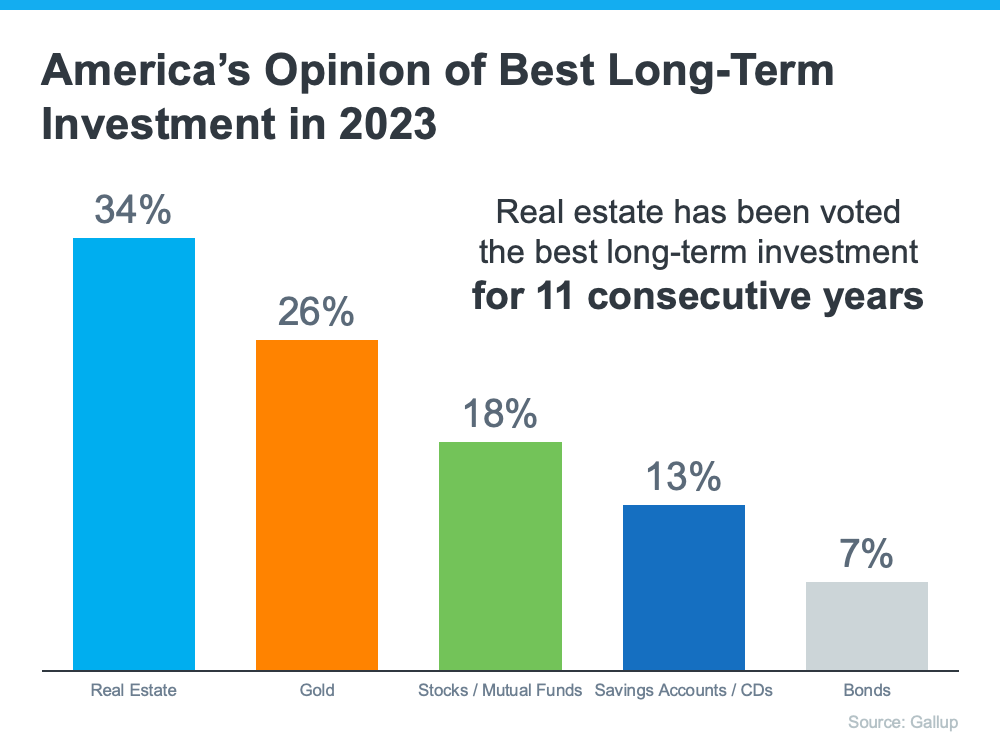

Real Estate Is Still Considered the Best Long-Term Investment

With all the headlines circulating about home prices and rising mortgage rates, you may wonder if it still makes sense to invest in homeownership right now. A recent poll from Gallup shows the answer is yes. In fact, real estate was voted the best long-term investment for the 11th consecutive year, consistently beating other investment types like gold, stocks, and bonds (see graph below):

If you’re thinking about purchasing a home, let this poll reassure you. Even with everything happening today, Americans recognize owning a home is a powerful financial decision.

Why Do Americans Still Feel So Positive About the Value of Investing in a Home?

Purchasing real estate has typically been a solid long-term strategy for building wealth in America. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), notes:

“. . . homeownership is a catalyst for building wealth for people from all walks of life. A monthly mortgage payment is often considered a forced savings account that helps homeowners build a net worth about 40 times higher than that of a renter.”

That’s because owning a home grows your net worth over time as your home appreciates in value and as you pay down your mortgage. And, since building that wealth takes time, it may make sense to start as soon as you can. If you wait to buy and keep renting, you’ll miss out on those monthly housing payments going toward your home equity.

Bottom Line

Buying a home is a powerful decision. So, it’s no wonder so many people view real estate as the best long-term investment. If you’re ready to start on your own journey toward homeownership, let’s connect today.

Today’s Real Estate Market: The ‘Unicorns’ Have Galloped Off

Comparing real estate metrics from one year to another can be challenging in a normal housing market. That’s due to possible variability in the market making the comparison less meaningful or accurate. Unpredictable events can have a significant impact on the circumstances and outcomes being compared.

Comparing this year’s numbers to the two ‘unicorn’ years we just experienced is almost worthless. By ‘unicorn,’ this is the less common definition of the word:

“Something that is greatly desired but difficult or impossible to find.”

The pandemic profoundly changed real estate over the last few years. The demand for a home of our own skyrocketed, and people needed a home office and big backyard.

Waves of first-time and second-home buyers entered the market.

Already low mortgage rates were driven to historic lows.

The forbearance plan all but eliminated foreclosures.

Home values reached appreciation levels never seen before.

It was a market that forever had been “greatly desired but difficult or impossible to find.” A ‘unicorn’ year.

Now, things are getting back to normal. The ‘unicorns’ have galloped off.

Comparing today’s market to those years makes no sense. Here are three examples:

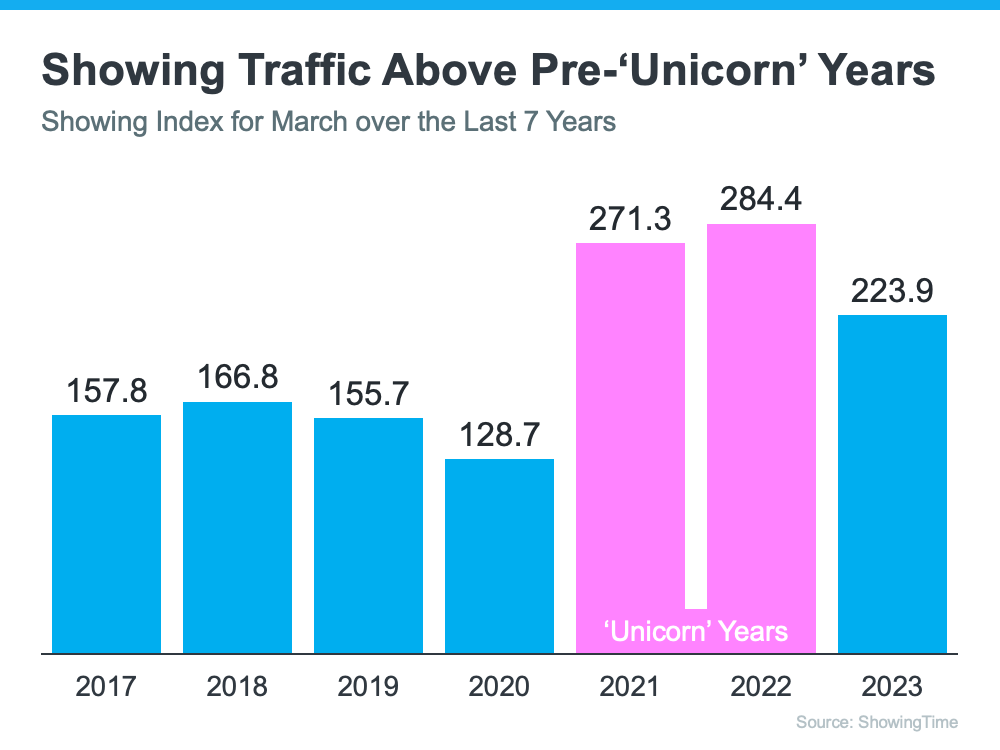

Buyer Demand

If you look at the headlines, you’d think there aren’t any buyers out there. We still sell over 10,000 houses a day in the United States. Of course, buyer demand is down from the two ‘unicorn’ years. But, according to ShowingTime, if we compare it to normal years (2017-2019), we can see that buyer activity is still strong (see graph below):

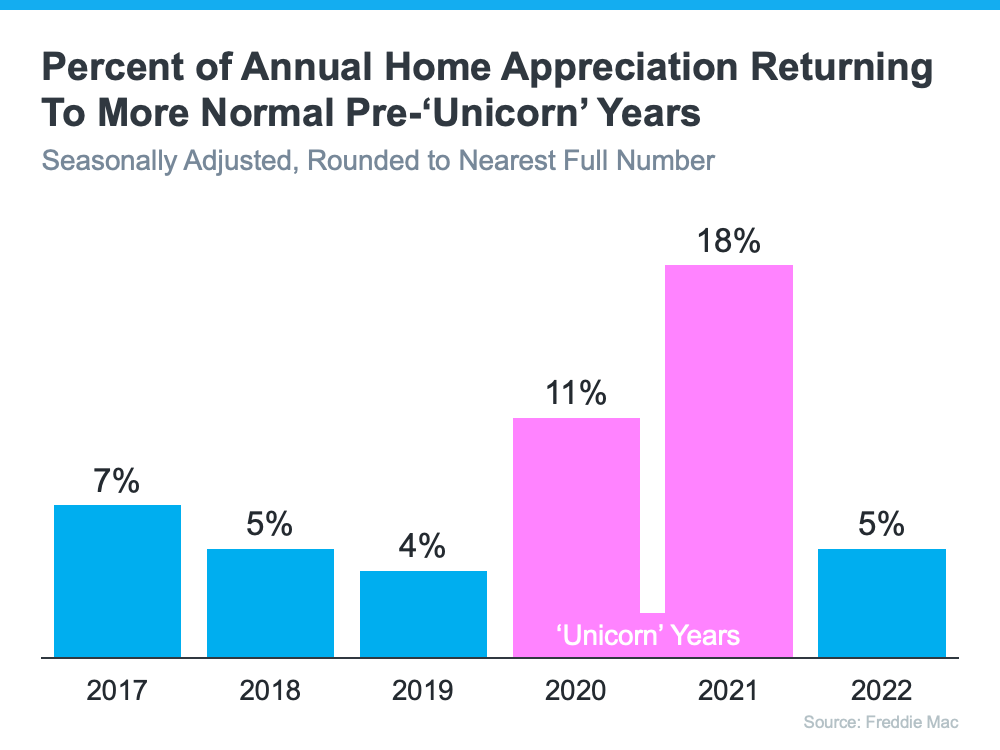

Home Prices

We can’t compare today’s home price increases to the last couple of years. According to Freddie Mac, 2020 and 2021 each had historic appreciation numbers. Here’s a graph also showing the more normal years (2017-2019):

We can see that we’re returning to more normal home value increases. There were several months of minimal depreciation in the second half of 2022. However, according to Fannie Mae, the market has returned to more normal appreciation in the first quarter of this year.

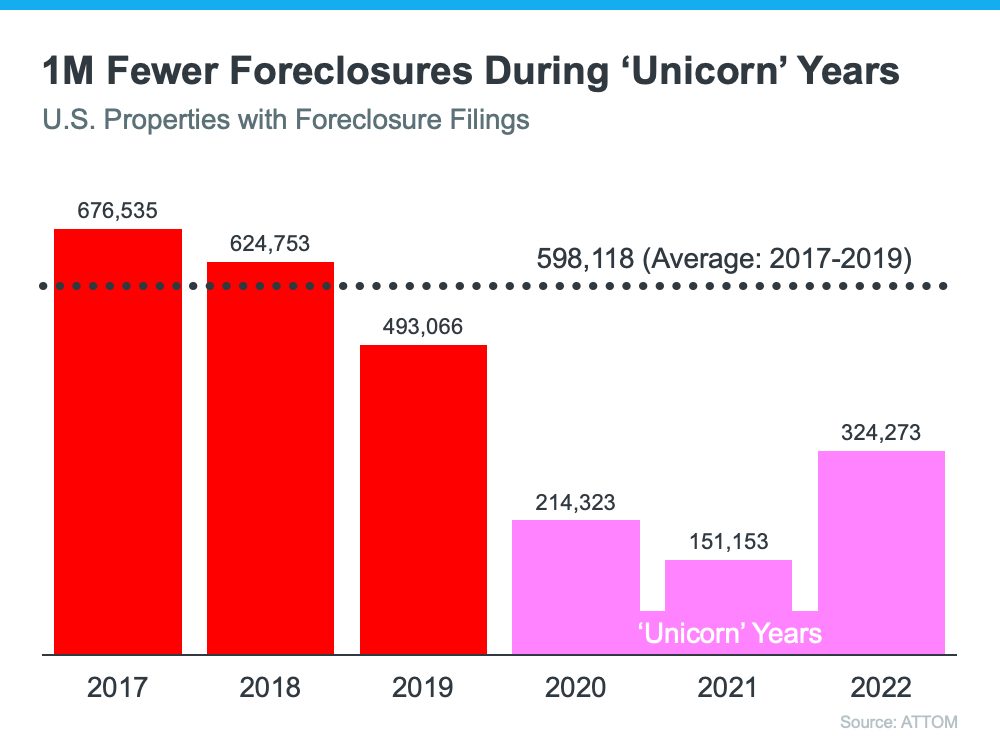

Foreclosures

There have already been some startling headlines about the percentage increases in foreclosure filings. Of course, the percentages will be up. They are increases over historically low foreclosure rates. Here’s a graph with information from ATTOM, a property data provider:

There will be an increase over the numbers of the last three years now that the moratorium on foreclosures has ended. There are homeowners who lose their home to foreclosure every year, and it’s heartbreaking for those families. But, if we put the current numbers into perspective, we’ll realize that we’re actually going back to the normal filings from 2017-2019.

Bottom Line

There will be very unsettling headlines around the housing market this year. Most will come from inappropriate comparisons to the ‘unicorn’ years. Let’s connect so you have an expert on your side to help you keep everything in proper perspective.

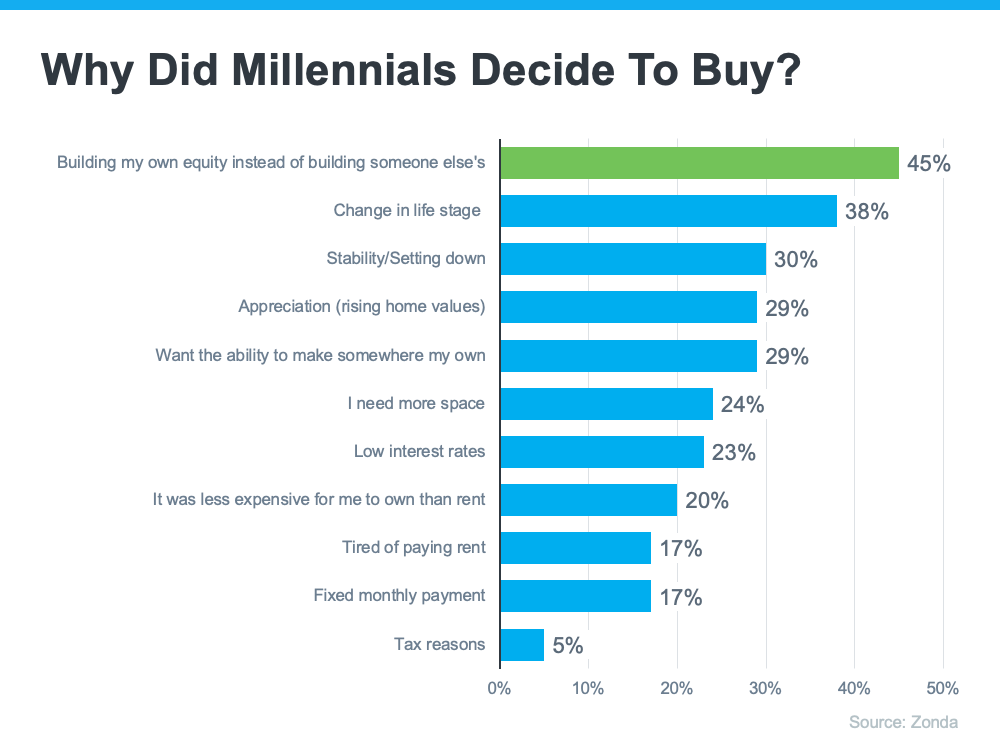

In the United States, there are over 72 million millennials. If you’re part of that generation and have thought about buying a home, you aren’t alone. According to Zonda, 98% of millennials want to become a homeowner at some point if they aren’t already. But why? There are plenty of reasons you may choose to become a homeowner. Here’s why other millennials have made that decision (see graph below):

This graph shows why millennials are buying homes according to Zonda’s 6th annual millennial survey. The top reasons include building equity, a change in life stage, wanting stability, rising home values, and wanting to make somewhere truly their own. Here’s a look at each in more detail.

Building equity – Homeownership is a long-term investment that allows you to build wealth, increase your net worth, and become more financially stable. Beyond that, the alternative to owning a home is typically renting. With the way rents have risen so dramatically over time, it may make sense to build your own equity instead of the equity of the person you’re renting from.

A change in life stage – As a millennial, you’re reaching your prime homebuying years. That means you may be at the point where you need more space or a different location.

Stability or settling down – This could mean establishing your career or just generally deciding more concretely what you want your life to look and feel like. As that idea becomes clearer, you may want to establish that lifestyle in a particular place and put down roots.

Rising home values – By purchasing a home, you own an asset that traditionally increases in value over time. That can mean your home will have a higher resale value if you decide to move again.

Wanting to make somewhere “mine” – Owning a home gives a sense of freedom because you can customize it however you want, make updates as you see fit, and be yourself in a place that’s solely your own.

Bottom Line

There are plenty of great reasons why millennials are buying homes today. If you’ve thought about becoming a homeowner and any of these reasons resonate with you too, let’s connect to explore your options.

Homeowners Have Incredible Equity To Leverage Right Now

Even though home prices have moderated over the last year, many homeowners still have an incredible amount of equity. But what is equity? In the simplest terms, equity is the difference between the market value of your home and the amount you owe on your mortgage. The National Association of Realtors (NAR) explains how your equity grows over time:

“Housing wealth (home equity or net worth) gains are built up through price appreciation and by paying off the mortgage.”

How Your Equity Can Help You Achieve Your Goals

The equity you build up over the years can be used to your advantage when you sell your current house and buy your next home. If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, your equity can be a powerful tool you can use to help you make a move in today’s market. That’s because it may be some (if not all) of what you need for your down payment on your next home.

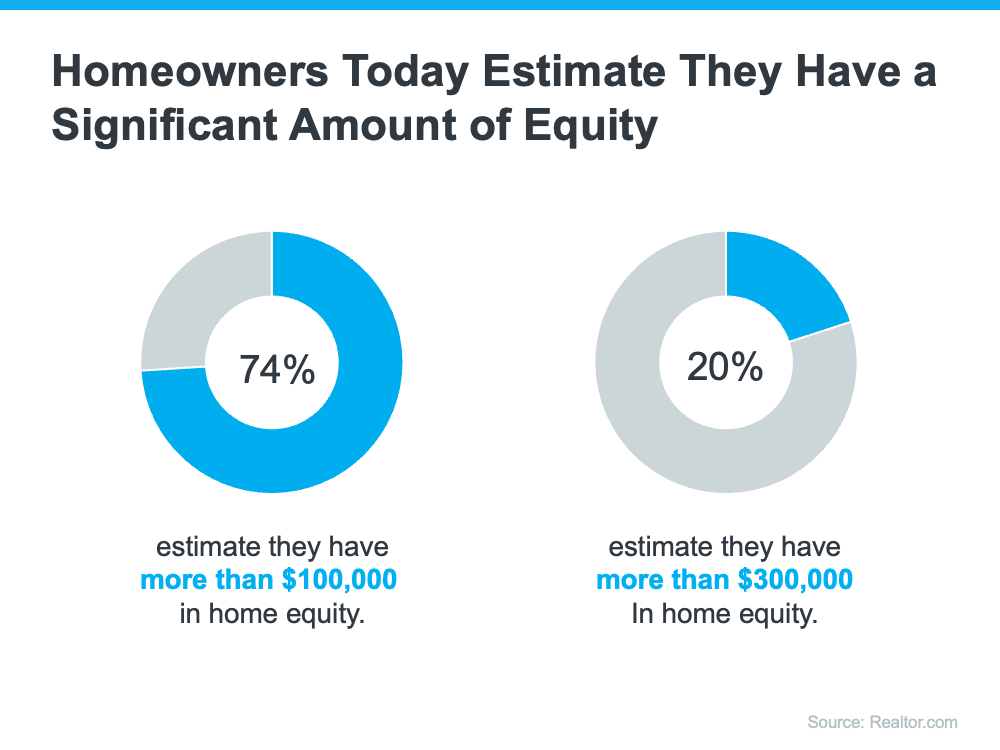

And how much equity you have may surprise you. A recent survey from Realtor.comfinds many homeowners today estimate they’ve built up a significant amount of equity:

The latest data from CoreLogic helps solidify why homeowners are feeling so good about the equity they’ve likely gained over time. As Selma Hepp, Chief Economist for CoreLogic, says:

“While equity gains contracted in late 2022 due to home price declines in some regions, U.S. homeowners on average still have about $270,000 in equity, nearly $90,000 more than they had at the onset of the pandemic.”

How a Skilled Real Estate Agent Can Help

If you’re looking to leverage your equity to boost your buying power in today’s market, having a trusted agent by your side makes a difference.

A real estate professional can help you better understand the value of your home, so you’ll get a clearer picture of how much equity you likely have. As a recent article from Bankratesays:

“Hiring a skilled real estate agent can give you a realistic estimate of home prices in your area and how to price your current home. Using that figure, you can calculate how much equity you have and what your net proceeds will look like, so you can apply that money toward the down payment and closing costs of your new home.”

Having a solid understanding of your equity is key when it comes to making decisions about buying or selling your home. A skilled agent can help you navigate the often-complicated process of selling your house and ensure the transaction goes smoothly.

Bottom Line

Today, many homeowners are sitting on a substantial amount of equity, and you may be one of them. Let’s connect so we can estimate how much equity you have and plan how you can use it toward the purchase of your next home.

If you’re looking to buy a house, you may find today’s limited supply of homes available for sale challenging. When housing inventory is as low as it is right now, it can feel like a bit of an uphill battle to find the perfect home for you because there just isn’t that much to choose from. If you need to open up your pool of options, it may be time to consider a newly built home.

According to the latest data from the U.S. Census, there’s positive news when it comes to new home construction. When you look at the first three months of this year, you’ll find:

More new homes were completed and are ready to sell. This gives you more move-in-ready options for your search.

Builders broke ground and started construction on more single-family homes. This means there are more homes intended for one household in the beginning stages of construction, allowing you the opportunity to customize one to your liking.

The number of permits for building new single-family homes ticked up. This shows builders are ramping up to start on even more home construction soon.

And, while this is all good news for broadening your options for your home search, there are other perks that come with considering a newly built home.

Customization

When you buy a new home under construction, you can tailor it to your unique needs and taste. Bankratesays:

“Building means customizing. . . . instead of wishing your home had a certain kind of flooring, a sunroom or some other special amenity, you’ll be able to tailor the property to your exact needs.”

Brand New Everything

Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

Minimal Repairs

And, because everything is new, you’ll likely find there are fewer maintenance and repair needs up front. As Realtor.com explains:

“. . . if something does go wrong with your new home, not only are there likely some manufacturer warranties in place, but many builders also include additional home warranties . . .”

Energy Efficiency

Lastly, building a home gives you the opportunity to incorporate more energy-efficient options that can help lower your costs over time – which can feel especially important when inflation’s raising many of the costs around you.

Bottom Line

If you’re having trouble finding your dream home in today’s market, it may be time to consider newly built homes as an option. Let’s connect so you have an expert on your side to help you explore what’s available in our local area.

The Three Factors Affecting Home Affordability Today

There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates climbed dramatically since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

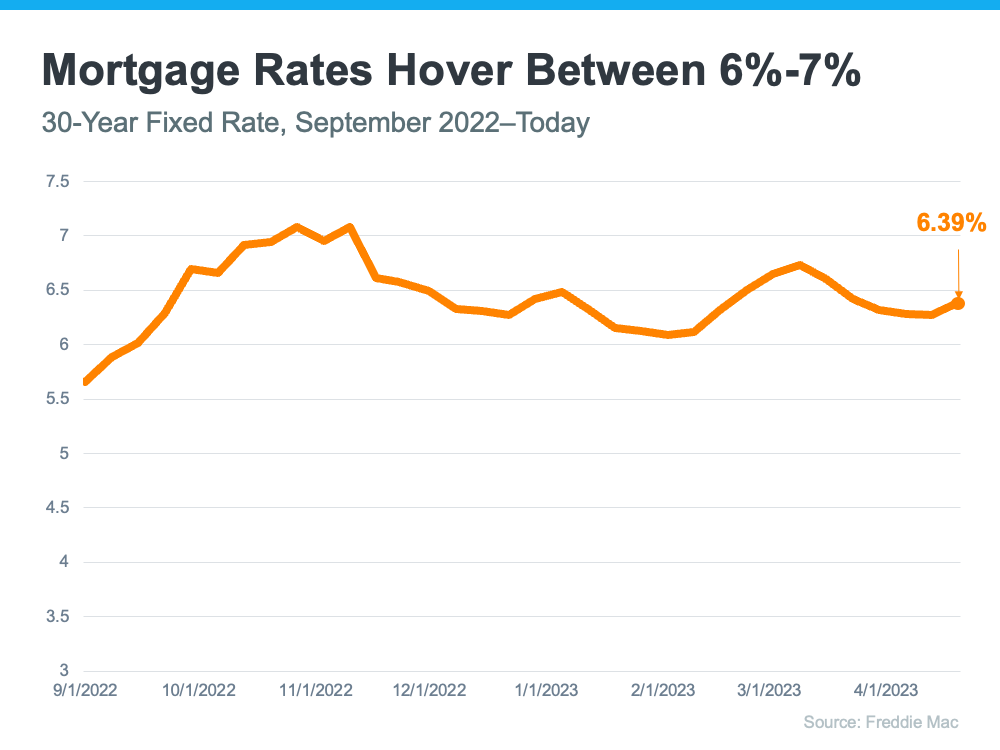

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

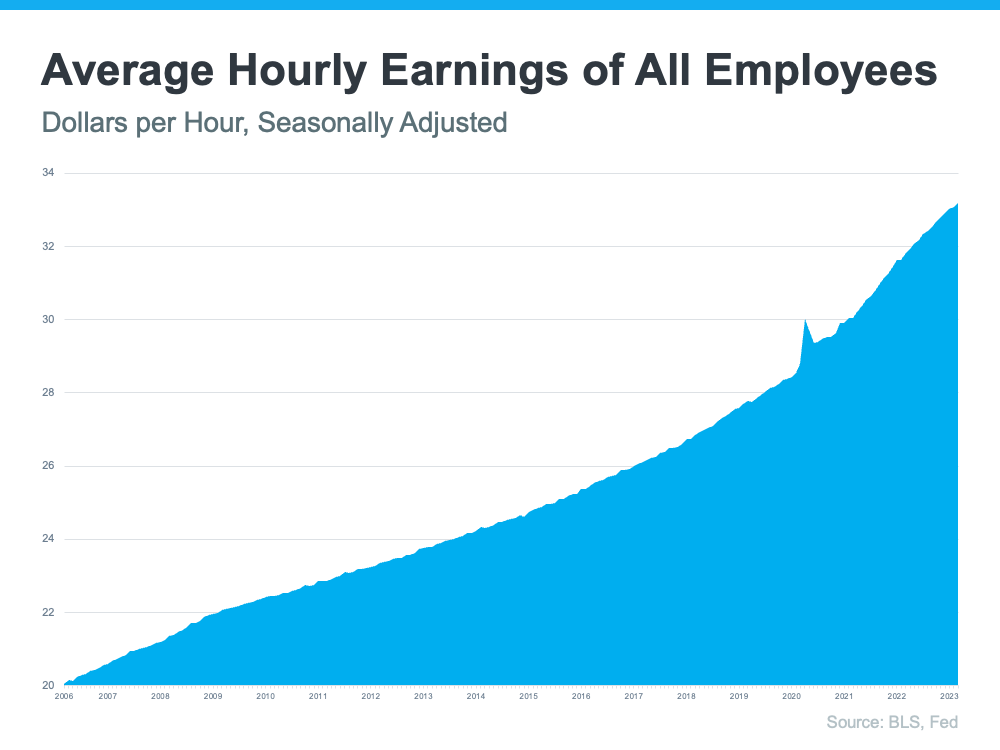

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage since you don’t have to put as much of your paycheck toward your monthly housing cost.

Home affordability comes down to a combination of rates, prices, and wages. If you have questions or want to learn more, reach out to a real estate professional who can explain what’s happening locally and how these factors work together.

Bottom Line

If you’re planning to buy a home, knowing the key factors that impact affordability is important so you can make an informed decision. To stay up to date on the latest on each, let’s connect today.

If you’re buying a home this spring, today’s housing market can feel like a challenge. With so few homes on the market right now, plus higher mortgage rates, it’s essential to have a firm grasp on your homebuying budget. You’ll also need a sense of determination to find the right house and act quickly when you go to put in an offer. One thing you can do to help you prepare is to get pre-approved.

To understand why it’s such an important step, you need to know what pre-approval is. As part of the process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow.

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow so you have a stronger grasp of your options. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

That’s not the only thing pre-approval can do. Another added benefit is it can help a seller feel more confident in your offer because it shows you’re serious about buying their house. And, with sellers seeing a slight increase in the number of offers again this spring, making a strong offer when you find the perfect house is key.

As a recent article from the Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. It lets you know what you can borrow for your loan and shows sellers you’re serious. Connect with a local real estate professional and a trusted lender so you have the tools you need to purchase a home in today’s market.

Your Tax Refund Can Help You Achieve Your Homebuying Goals

Have you been saving up tobuy a home this year? If so, you know there are a variety of expenses involved – from your down payment to closing costs. But there’s good news – your tax refund can help youachieve your goals by paying for some of these expenses.

SmartAssetestimates the average American will receive a $1,798 tax refund this year. The map below provides a more detailed estimate by state:

According toFreddie Mac, there are multiple ways your refund check can help you as a homebuyer. If you’re getting a refund this year and thinking about buying a home, here are a few tips to keep:

Saving for a down payment – One of the largest barriers to homeownership is saving for adown payment. You could reach your savings goal more quickly than expected by using your tax refund to help with your down payment.

Paying for closing costs – You have to pay fees to your lender, real estate agent, and other parties involved in the homebuying transaction before you can officially take ownership of your home. You could direct your tax refund toward theseclosing costs.

Lowering your interest rate – Your lender might give you the option tobuy down your mortgage interest rate during the homebuying process. That means, you could pay upfront to have a lower interest rate on your fixed-rate mortgage.

The best way toprepare to buy a home is to work with a trusted real estate professional who understands the process. They’ll help you navigate the costs you may encounter as youbegin your homebuying journey.

Bottom Line

Your tax refund can help you reach your goals of homeownership. Let’s connect to discuss how you can start your journey today.

3 Ways to Prioritize 11 Outdoor Remodeling Projects

With warmer weather on the horizon, many homeowners are gearing up for outdoor home improvements. But remodeling isn’t cheap. With thousands of dollars on the line, prioritizing projects is essential.

What’s the best way to set your priorities? The 2023 Remodeling Impact Report: Outdoor Features from the National Association of REALTORS® (NAR) Research Group examines three perspectives, using feedback from homeowners, real estate professionals, and landscape professionals.

The new report evaluates 11 outdoor remodeling projects, which can vary dramatically in size and scope. To help survey respondents provide consistent feedback, the project parameters were defined as follows:

1. In-ground pool addition – Install an 18-foot-by-36-foot in-ground pool with gunite walls, 3-foot to 7-foot depth, and a standard filtration system. Include a 3-foot-wide-by-4-inch thick concrete perimeter surround. ($90,000)

2. Landscape lighting – Installation of a standard 600W transformer and 20 LED lights. ($6,800)

3. New patio – Install a backyard 18-foot-by-16-foot concrete paver patio, dry set over compacted gravel and sand base. Paving material at $7 to $10 per square foot. ($10,500)

4. New wood deck – Build a 14-foot-deep-by-18-foot-wide wood deck attached to the house with a ledger. Decking, railing, and stair treads are constructed with cedar lumber. The stairs are 4 feet wide with an open riser. All cedar is finished with a clear deck sealer. The lower structure is covered with pine or fir lattice. ($16,900)

5. Fire feature – Install a dry stacked natural stone kit and gas burner with a 10-foot diameter flagstone patio. ($9,000)

6. Overall landscape upgrade – Install a front walkway of natural flagstone 3 feet wide and 30 feet long. Add two stone planters 6 feet long and 2 feet wide. Install five flowering shrubs and one deciduous 15-foot-tall tree. Mulch with landscaping bark. ($9,000)

7. Landscape maintenance – Annual mulch application, mowing of 2,835 square feet of lawn, pruning of shrubs, and planting approximately 60 perennials or annuals. ($4,800)

8. Irrigation system installation – Installation and management of irrigation system for a lawn that is 5,000 square feet. No boring is required. ($6,000)

9. Standard lawn care service – Includes six standard seasonal fertilizer and/or weed control applications on 5,000 square feet of lawn. ($415)

10. Tree care – Includes three applications of tree fertilizer, regular spraying, trimming, and pruning, as well as removing one 30-foot-tall tree. ($2,875)

11. Outdoor kitchen – Install one inset grill, stainless steel drawers, ice chest, sink, and 60 square feet of concrete countertop, made from veneered masonry stone. ($15,000)

Option 1. Joy Scores

Consumers remodel their homes for various reasons, and most are satisfied with the results. For example, after remodeling, owners report having a greater desire to be in their homes (68% of respondents), increased enjoyment in their homes (60%), feeling happy (52%), and feeling satisfied when they see their completed project (45%).

Consumers rated all 11 outdoor remodeling projects highly, with joy scores at or above nine on a 10-point scale. The top three projects were an in-ground pool addition (10), landscape lighting (10), and a new patio (9.9).

Even though the top three projects earned nearly identical joy scores, they differed significantly in terms of the most important result:

In-ground pool addition – Better meets homeowners’ needs (32%)

Landscape lighting – Beauty and aesthetics (45%)

New patio – Better functionality and livability (52%)

High joy scores play a crucial role in loving your home. But if you’re concerned about making wise financial decisions, it may be preferable to consider other methods for setting project priorities.

Option 2. Cost Recovery

Members of the National Association of Landscape Professionals (NALP) provided cost estimates for each project, averaging anonymous responses from national survey data. It’s important to note that every project is unique, and prices will vary depending on geographic region, property, and scope of work.

Remodeling typically improves a home’s resale value, but some projects provide a better cost recovery payback than others. Therefore, members of the National Association of REALTORS® were asked to define how much homeowners can recoup on each project upon selling a home.

Interestingly, the least expensive project—standard lawn care service ($415)—had the highest cost recovery (217%). In sharp contrast, the most costly project—in-ground pool addition ($90,000)—tied with a fire feature for the lowest cost recovery (56%).

Option 3. Recommended by REALTORS®

When a REALTOR® is representing a homeowner who wants to sell their property, the agent may suggest improvements to help the property attract a larger pool of buyers. Those recommendations often include outdoor remodeling projects.

(Note that the term REALTOR® is a registered collective membership mark that identifies a real estate professional who is a member of the National Association of REALTORS® and subscribes to its strict Code of Ethics.)

Among the 11 projects included in the report, REALTORS® were most likely to recommend landscape maintenance (74%), standard lawn care service (53%), and tree care (44%). Landscaping-related projects may not earn the highest joy scores among homeowners, but they can dramatically improve a property’s curb appeal and suggest that the home is well maintained.

REALTORS® were least likely to recommend an irrigation system installation (2%), a fire feature (2%), an in-ground pool addition (1%), or an outdoor kitchen (1%).

Written by:

REBAC Staff. “3 WAYS TO PRIORITIZE 11 OUTDOOR REMODELING PROJECTS.” Homebuying.realtor, Real Estate Buyer’s Agent Council of the National Association of REALTORS®, 27 Mar. 2023, https://homebuying.realtor/content/3-ways-prioritize-11-outdoor-remodeling-projects?_cldee=r7GXExEInjU7KLhX3b96_JuNoZ0J3N9LufmZa0FDiL9A5i7ErF3qrEwlfRpLTZc2&recipientid=contact-302c93e0153b401db91dce54710dd0d7-4b448514dd474bca8fea8367a7242f16&esid=0c032dde-7ad9-ed11-9c76-00155d234439. Accessed 14 Apr. 2023.

There have been a lot of shifts in the housing market recently. Mortgage rates rose dramatically last year, impacting many people’s ability to buy a home. And after several years of rapid price appreciation, home prices finally peaked last summer. These changes led to a rise in headlines saying prices would end up crashing.

Even though we’re no longer seeing the buyer frenzy that drove home values up during the pandemic, prices have been relatively flat at the national level. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), doesn’t expect that to change:

“[H]ome prices will be steady in most parts of the country with a minor change in the national median home price.”

You might think sellers would have to lower prices to attract buyers in today’s market, and that’s part of why some may have been waiting for prices to come crashing down. But there’s another factor at play – low inventory. And according to Yun, that’s limiting just how low prices will go:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

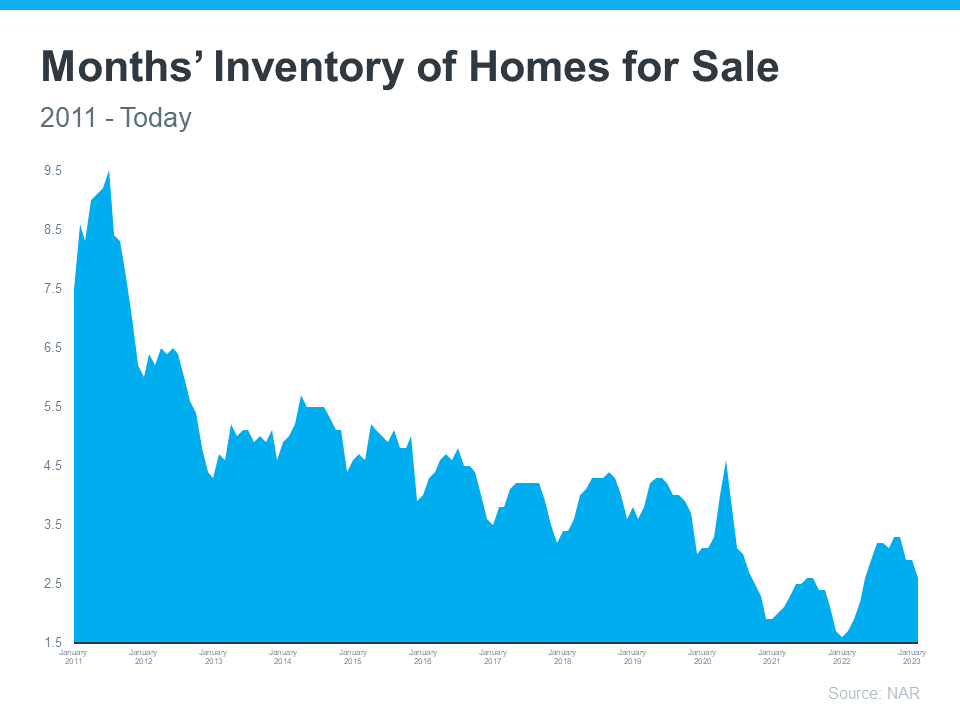

As you can see in the graph below, we’ve been at or near record-low inventory levels for a few years now.

That lack of available homes on the market is putting upward pressure on prices. Bankrateputs it like this:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

If more homes don’t come to the market, a lack of supply will keep prices from crashing, and, according to industry expert Rick Sharga, inventory isn’t likely to rise significantly this year:

“I believe that we’re likely to see low inventory continue to vex the housing market throughout 2023.”

Sellers are under no pressure to move since they have plenty of equity right now. That equity acts as a cushion for homeowners, lowering the chances of distressed sales like foreclosures and short sales. And with many homeowners locked into low mortgage rates, that equity cushion isn’t going anywhere soon.

With so few homes available for sale today, it’s important to work with a trusted real estate agent who understands your local area and can navigate the current market volatility.

Bottom Line

A lot of people expected prices would crash this year thanks to low buyer demand, but that isn’t happening. Why? There aren’t enough homes for sale. If you’re thinking about moving this spring, let’s connect.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link