Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

For a while, buying your first home hasn’t just felt hard. It may have felt out of reach.

Not because you weren’t ready.

Not because you weren’t trying.

But because every time you ran the numbers, they didn’t work.

That’s why so many first-time buyers stepped back.

But after years of sitting on the outside looking in, this Spring could give buyers like you an opening again – especially in some markets.

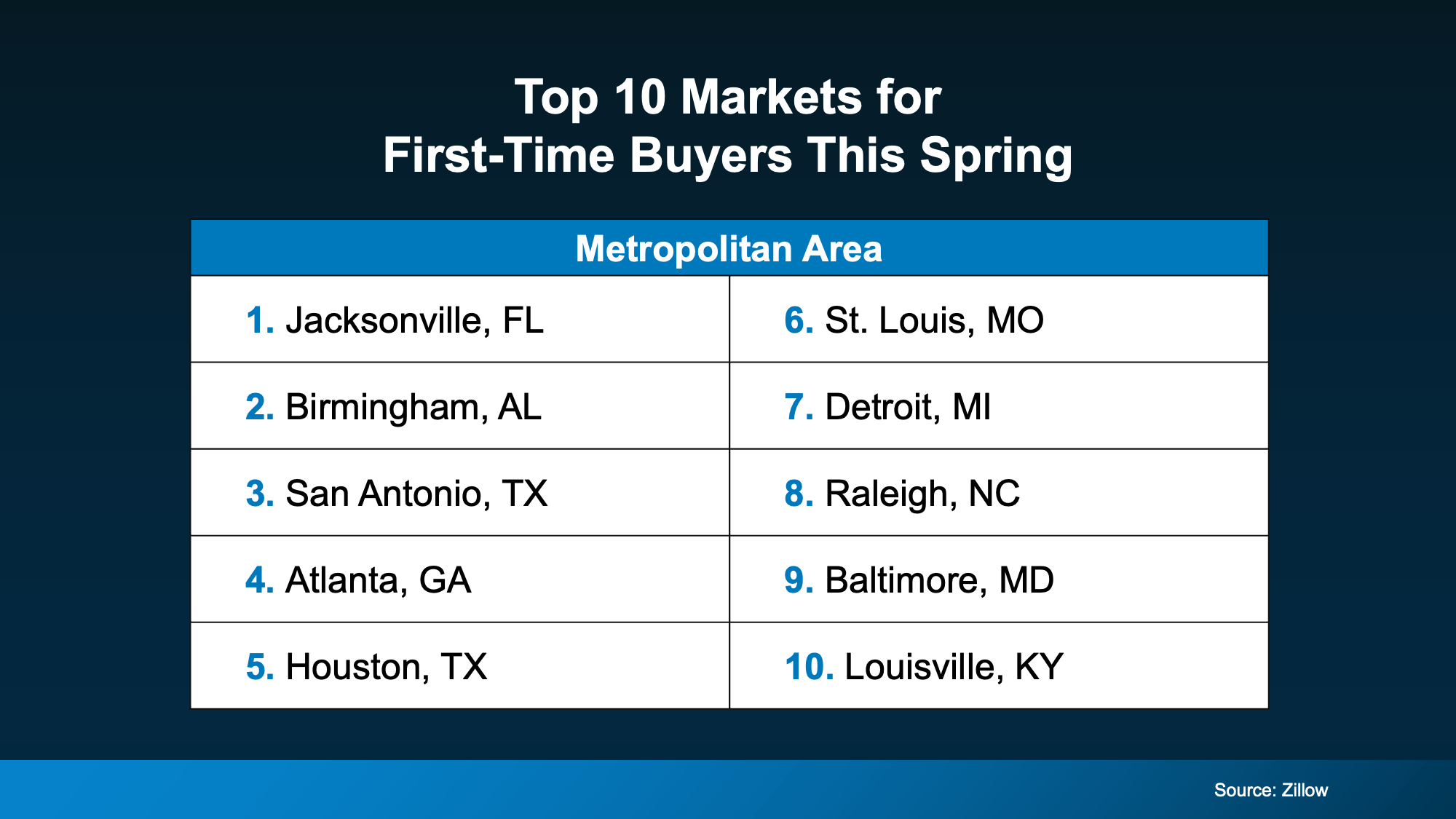

Metros Where Buyers May Have an Easier Time Breaking into the Market

Zillow just released a list of the top 50 metros for first-time buyers this Spring. And here’s a quick snapshot of the top 10 (see chart below):

According to Zillow, in these top-ranked markets, median-income households can afford 68% of all homes for sale. Let that sink in.

Not long ago, it felt like you could barely afford anything.

Now, you may actually have some options again.

That doesn’t mean every home is suddenly going to fit your budget. But it does mean the door that felt closed for so many buyers is starting to crack back open. And in a number of cities, first-time buyers may finally be getting a shot at buying.

Why This Is Starting To Open Up

These cities are rising to the top not because of any one big change, but from a few smaller ones finally lining up. As Orphe Divounguy, Senior Economist at Zillow, explains:

“First-time buyers are finally seeing some light at the end of the tunnel. Affordability is still a challenge, but rising incomes, stabilizing prices and improving inventory are creating real opportunities in parts of the country. In the strongest markets for first-time buyers, they’ll find more choices, less competition and a clearer path to homeownership than they’ve had in years.”

Basically, three big things are working in your favor:

- More homes are hitting the market. Realtor.com says inventory is up 8.1% compared to last year. That gives you more choices, less pressure, and more chances to find a place that fits your budget.

- Price growth is moderating, so homes aren’t moving further out of reach as quickly. Some may even be falling back within your target price point.

- Incomes are rising. If you make more money, that can offset some of the affordability challenges too.

And even though mortgage rates have been higher lately, that combination can still make a difference. As Mark Fleming, Chief Economist at First American, explains:

“Income growth has outpaced house price growth for 19 straight months, boosting house-buying power even as mortgage rates remain elevated.”

How To Find the Opportunities in Your Local Market

But what if your city didn’t make the top 10 list, or even the top 50 markets? Here’s what you really need to remember.

There’s going to be opportunities in every market, if you know where to look.

Even in the same city, two buyers can have completely different experiences. And a big part of that is who they choose as their partner. The right agent knows how to find pockets of opportunity in any market. That could mean:

- A neighborhood where prices haven’t climbed as quickly

- A part of town with more inventory, or

- A new build community offering incentives so builders can sell their inventory

So, even if your city didn’t make the list, that’s okay. There’s still an opening for you, you just need your agent to help you find it.

Bottom Line

For a long time, first-time buyers have felt stuck, waiting for their turn to buy. But for some buyers, this Spring might be the first time in a while where things start to feel more within reach again.

Want to see which neighborhoods could give you the best shot at buying right now? Let’s talk.